The Beyond the Grid Fund for Africa (BGFA) is an innovative SDG7 financing programme managed by Nefco. BGFA is now a EUR 126 million programme, funded by Denmark, Germany, Norway and Sweden that supports off-grid energy companies across Sub-Saharan Africa. These companies operate in solar home systems (SHS), mini-grids, productive use of energy (PUE) and battery rental value chains.

BGFA contracted Open Capital Advisors (OCA) to undertake an early assessment of the financial mobilisation aspects of the BGFA programme, with a particular focus on leveraging private capital.

Unveiling the divide: Energy access challenges in Sub-Saharan Africa

As global economies march towards the 2030 deadline for achieving SDG 7 – ensuring affordable, reliable, sustainable and modern energy for all – Sub-Saharan Africa faces a daunting challenge; approximately 600 million people, 53% of the population, still lack access to electricity. This is one of the most significant development challenges on the continent today. To achieve universal access by 2030, Sub-Saharan Africa faces a considerable funding gap, with only USD 426 million allocated to the off-grid energy sector in 2023, a meagre figure compared to the annual funding need of USD 28 billion.

Off-grid energy companies, which provide energy products not connected to or served by public or private energy utilities – such as SHS, mini-grids, PUE solutions and battery rentals – are crucial for achieving SDG 7 and combating climate change. However, accessing financing to scale their operations and reach underserved communities remains a significant challenge, especially for early-stage ventures lacking the track record to attract investors. Recent macroeconomic challenges, including depreciating currencies, high interest rates and inflation, compound the issue. Additionally, local financial institutions often lack a deep understanding of the sector, while dwindling investor confidence in certain off-grid value chains, such as SHS, has made equity financing scarce. These factors serve to widen the funding gap, especially for early-stage companies, hindering their ability to scale and address barriers to energy access. Additionally, nascent value chains, such as PUE and battery rental, face an overall lack of investment.

Delving into value chain-specific trends within the BGFA portfolio reveals additional insights: mini-grids, for instance, need substantial upfront investment and access to project financing, which can take time to secure. Challenges in the regulatory environment can further complicate the licensing process, and the absence of clear regulatory guidance can create uncertainty for developers, affecting their ability to forecast returns and access necessary financing. Furthermore, there is a significant shortage of long-term financing options, making it difficult for developers to secure the capital needed for sustainable projects. For SHS companies, prioritising pay-as-you-go (PAYGo) models is crucial for ensuring affordability for customers. However, despite initial investor interest in funding PAYGo models, the lack of success stories within the SHS value chain has amplified the perceived risks, making investors reluctant to commit to equity investments. PUE and battery rental are both nascent sectors, and therefore have largely not received significant investment yet, although there are some exceptions. In general, investors are adopting a cautious approach as they gain a deeper understanding of these value chains.

Propelling progress: BGFA makes positive strides in enabling capital mobilisation to the off-grid energy sector

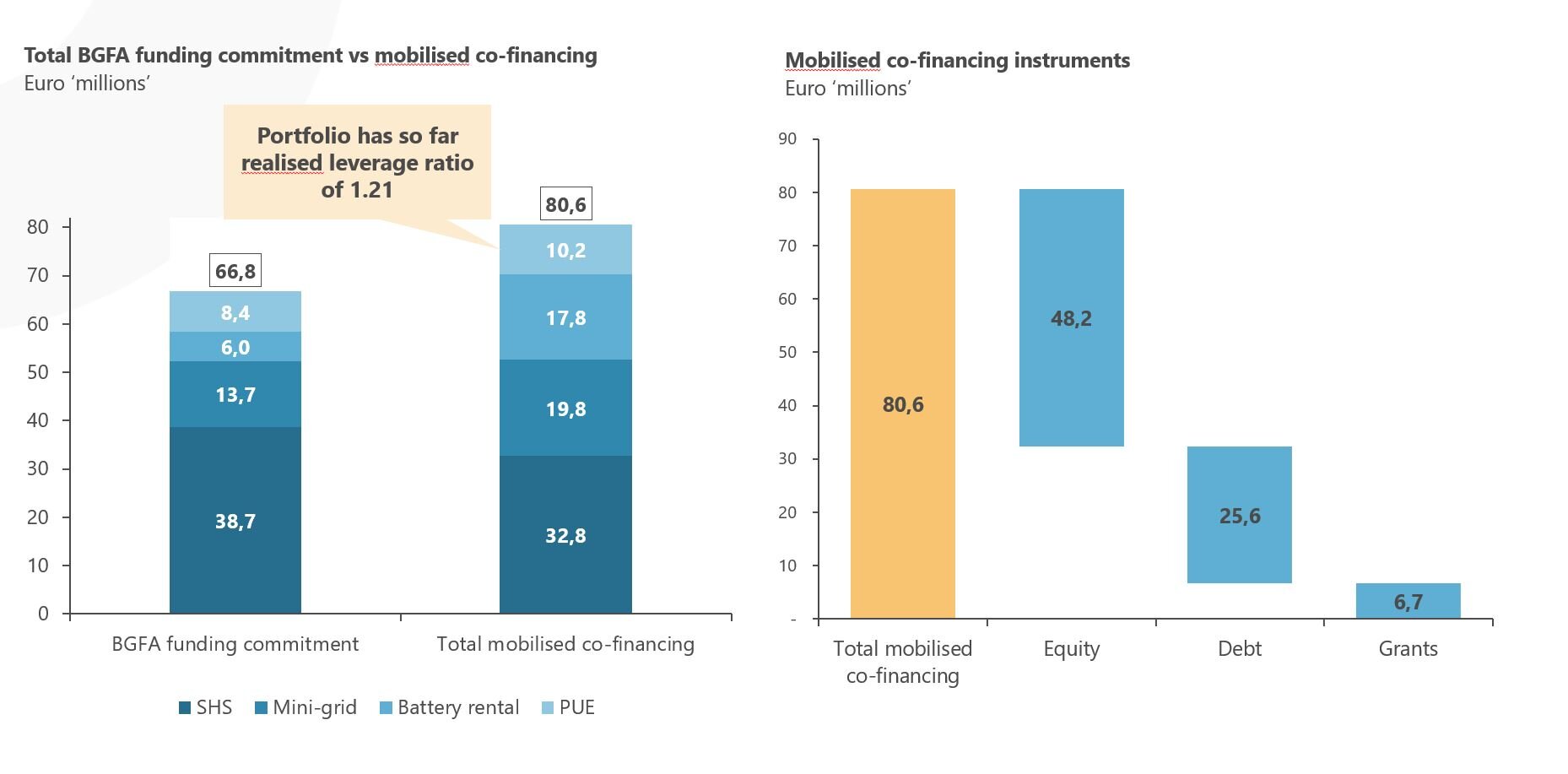

BGFA continues to play a crucial role in the off-grid energy sector by supporting its portfolio companies, enabling them to mobilise additional capital from private investors. To date, BGFA has committed ~EUR 67 million in funding to enable companies to ensure the affordability of their products or services, expand their customer bases and enter new markets. Funding has been deployed across Sub-Saharan Africa, with Southern, East and West Africa receiving 54%, 27% and 19% of total funding, respectively. SHS companies make up more than half of the BGFA portfolio and, as such, have received 58% of funding commitments, reflecting the relative maturity of the SHS value chain compared to the other three in the portfolio.

OCA found that BGFA funding has played a catalytic role for portfolio companies in various aspects:

- Enabling scale: Advance payments facilitate market entry, inventory procurement and the establishment of sales and distribution networks, helping to provide the necessary traction to attract potential investors.

- Improving revenue opportunities: The traction achieved through scale helps drive revenue growth for companies.

- Boosting credibility: BGFA fundingand milestone achievements serve as positive signals for investors, enhancing credibility in the investment landscape.

- Enhancing fundraising effectiveness: Technical assistance (TA) provided by the programme helps companies refine their processes and policies. Addressing priority areas, such as gender and e-waste policies, not only improves operations and promotes adoption of best practices but is also important for attracting capital, especially from impact-focused investors.

These strategies have contributed to the success of BGFA portfolio companies in mobilising additional financing to further address energy access challenges in Sub-Saharan Africa. By April 2024, 20 of the 29 companies in the portfolio had successfully mobilised EUR 80.6 million in additional financing, mainly as private capital from international sources. This resulted in a realised leverage ratio of 1.2 within less than 2 years of partaking in the programme, against a target of 3-4 years. Notably, however, 52% of this funding was mobilised by only six companies.

Looking ahead, portfolio companies plan to mobilise even more capital to continue scaling. Most companies expect forthcoming funding to be largely in the form of debt, whereas most funding to date has been mobilised through equity. Should the funding rounds that are currently planned and under negotiation close successfully, the realised leverage ratio of the portfolio would increase to 5.1x, further underscoring the substantial impact of BGFA on the financial mobilisation efforts of its portfolio companies.

Addressing the void: The funding challenge ahead

While the investors interviewed during the course of the study acknowledged that results-based funding (RBF) promotes confidence by reducing perceived investment risks, they emphasised the importance of off-grid energy companies demonstrating their sustainability without the support of grants. This underscores the essential role of other types of financing in enabling companies to reduce their reliance on grants, allowing them to gain traction and scale faster than through RBF funding alone.

OCA found that different off-grid energy value chains present distinct funding and TA requirements, emphasising the need for a comprehensive approach, in addition to RBF funding:

- Mini-grids serving rural and hard-to-reach customers require subsidies to rationalise project costs and ensure economic sustainability. In addition to subsidies, mini-grids require more patient equity financing to foster long-term growth. Multiple projects need to be run concurrently for optimal and sustainable operations, requiring more funding than is currently available via the market. From a business model perspective, businesses require TA to better integrate PUE into their operations and thus improve their customers’ payment capacity and the financial sustainability of projects.

- SHS companies continue to require subsidies to cater to underserved customers and new markets and equity to scale more effectively.

- PUE companies need subsidies to scale and reduce product prices to improve adoption rates. Moreover, they require TA support to access carbon credit markets and R&D funding to diversify and improve their product offerings.

- Battery rental companies require TA to align their practices with sustainable battery use and disposal. Additionally, R&D funding is essential to produce higher capacity battery packs and expand revenue streams, particularly in emerging sectors like e-mobility.

Alongside the support provided by RBF funding, stakeholder collaboration is essential in developing tailored and practical solutions to effectively address these needs. Broad market intervention opportunities identified include:

- Need for more early-stage investors to offer concessional and patient capital to support early-stage companies, particularly in underserved markets, enabling them to launch/scale activities. Donor-funded programmes should increase PUE financing facilities in particular and explore integrated financing initiatives across various technological value chains, like providing PUE appliance financing to mini-grid customers, to address limited funding availability. The BGFA will soon launch a funding window in Mozambique focused exclusively on PUE.

- Multi- and bilateral donors should collaborate more with local financial institutions, offering sector-specific knowledge and capacity building to facilitate crowding in of new investors. Partnering with experienced investors to lead investments and allowing local financial institutions to follow, as well as providing credit guarantees, can attract more investors and mobilise local funds. Donor programmes should also facilitate cheaper and more accessible FX hedging options/platforms for seed and start-up companies, while targeted awareness campaigns remain crucial for mobilising new capital providers and scaling nascent sectors like PUE and battery rental.

- TA in the sector should be structured to provide long-term support and offer extended or multiple support packages tailored to companies’ evolving capital needs across different growth stages, rather than one-off interventions for single capital raises. Moreover, stakeholders should regularly organise industry events to foster networking among off-grid energy companies, investors and key market players, promoting collaboration and knowledge exchange.

- Donor-funded programmes should collaborate to disseminate best practices and industry insights, while also aiding governments in formulating and enacting supportive regulatory policies. This includes initiatives like cost-reflective tariffs, repayment guarantees for mini-grid developers facing utility expansion, standardisation mechanisms for PUE and duty exemptions for a wide array of SHS products. Additionally, companies should maintain active engagement with BGFA’s Off-Grid Task Forces in their respective countries, ensuring alignment with government initiatives and optimising the effectiveness of these task forces.

- Multi- and bilateral donors should explore off-balance sheet facilities to buy receivable portfolios of small and medium-sized companies, reducing their need for working capital. Donor programmes could also provide carbon market TA for companies to diversify revenue through carbon credit sales. Additionally, by collaborating with governments, donors can increase public funding for mini-grid projects to improve project viability and lower tariffs for customers. Finally, promoting value chain partnerships among energy service providers can reduce funding needs by allowing companies to focus on core competencies, such as mini-grid developers partnering with battery rental companies to improve project viability without requiring appliance financing.

Nefco would like to thank the OCA team which undertook the study for BGFA: Lornah Gacheri, Duda Slawek, Chileshe Lungu, Vidur Dhingra and Jason Gikonyo.

For further information:

Read and download the report Financial mobilisation and financing trends for more information.